Switch Metals: Rare Tantalum Mining Investment Opportunity with Lithium upside

AIM listed Switch Metals is focused on the rare critical mineral known as Tantalum, with Lithium upside. Tantalum is critical to a number of industries, particularly aerospace and defence. Switch are operating in Côte d’Ivoire—an underexplored but increasingly attractive mining jurisdiction in West Africa and most importantly—an alternative supplier to that of Rwanda and the DRC where up to 70% of global supply originates from despite significant ESG and traceability risk.

Overview

Switch Metals (AIM: SWT) is a London-listed exploration company focused on developing critical mineral assets in Côte d’Ivoire, a highly prospective and increasingly attractive mining jurisdiction in West Africa.

The company is the largest critical metals landholder (+3,000 km2) in Côte d’Ivoire and is primarily focused on Tantalum, a rare critical mineral with supply constraints led by Rwanda and the DRC accounting for up to 70% of its global supply. Despite Tantalum being the company's core focus, a recent spodumene lithium discovery in Feb 2026 adds further upside to Switch's critical metals portfolio.

Côte d’Ivoire is a stable mining jurisdiction benefitting from:

- Good Infrastructure (power, water, roads and mineral ports)

- Presence of major international miners

- Business friendly with strong economic growth

- Highly prospective Geology

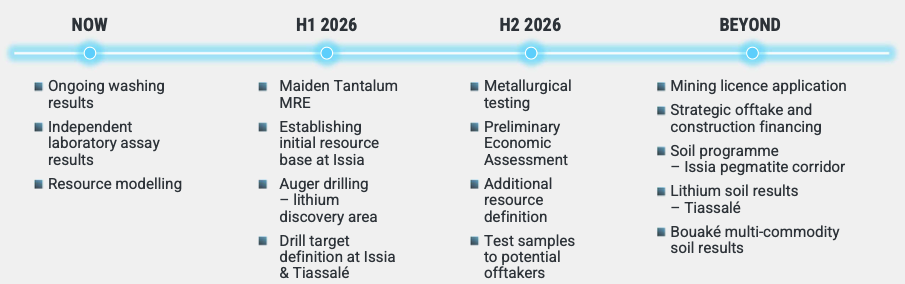

The company is rapidly executing its Phase 1 work programme with an initial Maiden Resource Estimate ("MRE") due shortly.

Why Tantalum ?

Tantalum is a critical component in high-performance electronics, particularly capacitors used in smartphones, automotive systems, aerospace applications, medical devices, you name it! It's essential for modern electronics and has a number of unique characteristics such as an extremely high heat tolerance and can store and release electrical energy very efficiently, which makes it essential in compact, high-performance devices.

It's Geologically rare as its typically found in complex pegmatites alongside lithium, making deposits difficult to locate and define. Not only is Tantalum rare (at least in terms of economically viable deposits) but there are significant supply risks due to around 70% of the worlds current supply coming from Rwanda and the DRC. These are well known conflict zones meaning supply could be impacted at any time. Furthermore, supply from these regions brings ESG and traceability concerns.

Due to the factors above, Tantalum has been trading as high as US$275,000 per tonne and with the likes of multiple wars and the resultant increase in global defence spending, the outlook for Tantalum remains strong, especially with on-going supply risks.

This means new discoveries and development projects—especially in stable jurisdictions such as Côte d’Ivoire —can be highly valuable.

Projects

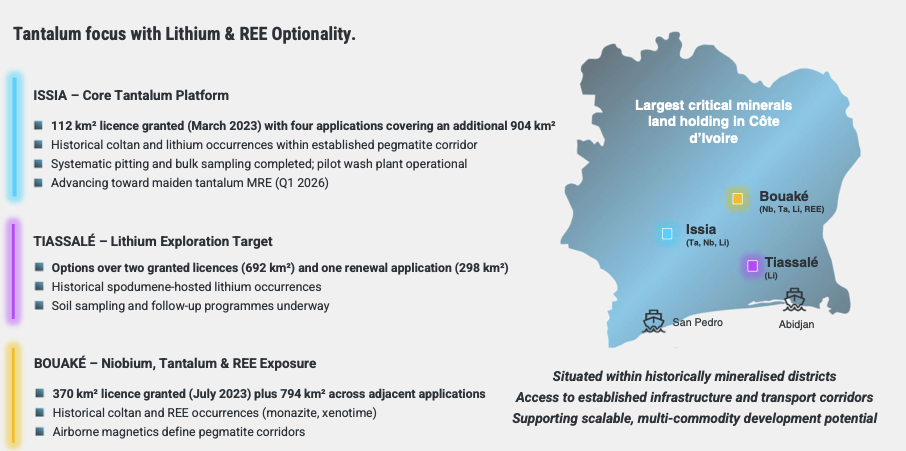

Project Portfolio (Source:Switch Metals)

As seen above, Switch has a strong portfolio of projects accross key critical minerals with exploration upside but for the purpose of this article, we will focus on Issia, the company's core Tantalum focused project with additional Lithium upside.

ISSIA

Issia is the company's core Tantalum project, and the company plans to phase its development as follows:

Phase 1 - Near-term value drivers

Issia hosts several near-surface targets both Eluvial and Colluvial Coltan (Ta + Nb)—Coltan is the collective word for Tantalite (Tantalum) and Columbite (niobium). It's a dull black metallic ore from which both elements can be extracted.

By focusing on these targets first, the company can move forwards with development, establishing its maiden MRE (expected shortly) and then rapidly move on to metallurgical testing, production of a Preliminary Economic Assessment ("PEA") and the provision of bulk samples to potential off takers.

The company is already well advanced with Phase 1 having excavated 369 pits, resulting in 400 tonnes of stockpiled ore, ready for wash and processing. The Pilot Plant is already operational and producing coltan concentrate ready for bulk testing.

The output of Phase 1 will be the company's MRE— with product ready for testing.

Phase 2 - Growth

Phase 2 at Issia focuses on unlocking longer-term growth potential through systematic hard-rock exploration across priority pegmatite targets. Further drilling will then be done to advance successful targets towards resource definition. This takes the company beyond resource for the near-surface targets to increase the overall resource.

Lithium Upside

Earlier in the year, Switch announced a new lithium discovery from a spodumene bearing pegmatite at Issia.

Initial results from reconnaissance and sampling identified lithium-bearing pegmatites at surface, confirming the presence of a prospective lithium system. The mineralisation looks to be consistent with hard-rock spodumene-style deposits.

Grades range from 1.00% to 2.58% lithium oxide ("Li2O") which were tested on spodumene-rich zones using a portable Laser-Induced Breakdown Spectroscopy analyser (pLIBS).

Following the discovery, Switch will look to accelerate the work at Issia on this new lithium prospect in parallel to the ongoing tantalum MRE

Investment Case

Rare Tantalum Focused Development

Switch Metals offers investors a rare opportunity to gain exposure to an early-stage Tantalum focused junior mining company. As explained earlier in the article, Tantalum supply is constrained and Switch as a future producer should benefit from superior ESG credentials which could likely result in premium pricing.

Diverse Critical Minerals Exposure

As well as its core focus on Tantalum, Switch has derisked its portfolio through a Lithium discovery—with other Lithium projects within its overall portfolio. With the ongoing concerns around the reliance on critical minerals from China, Switch is well placed to capitalise on its Critical Minerals portfolio

Aligned & Experienced Management

The Switch Management team are experienced with in-country presence. CEO and Co-founder, Karl Akueson and the Board collectively hold over 10% in the company.

Stable Jurisdiction

Côte d’Ivoire is an attractive mining jurisdiction due to its political stability, pro-investment mining code, and improving infrastructure. The government actively supports exploration and foreign investment, while established gold operations demonstrate a functioning regulatory framework.

Its underexplored geology offers significant upside, particularly for critical minerals, making it a compelling destination for early-stage resource companies such as Switch.

Early in the Value Curve

2026 Work Programme (Source: Switch Metals)

As Switch is essentially early-stage i.e. discovery and exploration and moving into development, its implicitly early in the value curve. As the company delivers its Maiden Resource and subsequently increases that resource its valuation should typically increase.

In addition, through 2026 the company intends to deliver its Preliminary Economic Assessment ("PEA") and secure its mining license. These key steps in addition to establishing a rare and high-margin Tantalum resource (with Lithium upside) should further have a positive effect on its valuation.

Staged Approach

Switch's staged and phased approach with its initial free dig, gravity recovery and no crushing operation can—upon mining license approval—allow the company to execute a low capex, high margin, short payback operation that should then allow the company to grow organically and expand its resource with a view to ramping up to a much larger mining operation, especially given it's the largest critical minerals landholder in the Côte d’Ivoire

Financing Optionality

Switch as a listed company on the AIM has access to the Capital Markets and can obviously raise cash through the issuance of equity as and when required, however, Switch late last year struck an MOU with Xcelsior Capital that outlines the key terms for a proposed strategic partnership between the parties.

Xcelsior provides flexible financing solutions for critical minerals company's helping them secure exploration, development and capex funding—importantly, the MOU should give Switch optionality when it comes to funding, and provide an alternative to equity dilution.

An Eye on Risk

As With any junior mining company, there are a number of risks investors should consider, some as follows:

Funding: As an early-stage company, Switch will need to secure progressive funding to drill and increase resource, to operate its pilot wash plant and produce samples for testing, complete the PEA and cover general G&A. This is mitigated by the fact the company is listed and has access to the Capital Markets along with its relationship with Xcelsior and the possibility of grant funding from the likes of the US DFC who support critical minerals projects in Africa.

Jurisdictional: Africa is generally considered a higher risk jurisdiction, however investment in Africa is increasing with a number of successful projects in place. Côte d’Ivoire is an attractive mining jurisdiction due to its political stability, pro-investment mining code, and improving infrastructure.

Commodity Risk: Switch are focused on Tantalum with potential Lithium upside. The demand/supply dynamics could affect the price of each commodity. However, this is somewhat mitigated by the fact that Switch should have superior ESG credentials and importantly for potential off takers—product traceability. Switch is not directly exposed to one metal given its Tantalum and Lithium portfolio, both of which are classified as Critical Minerals.

Conclusion

Switch Metals offers investors a rare opportunity to gain exposure to an early-stage Tantalum focused junior mining company with potential Lithium upside. Switch's portfolio offers diversity, and the company is the largest critical minerals landholder (+3,000 km2) in Côte d’Ivoire—a stable and pro-mining jurisdiction.

Being early stage but with a near-term fast track plan to early production, if Management execute, investors can benefit from progressive de-risking milestones that should incrementally increase the company's valuation.

Switch is marketing itself as an ethical, long-term stable supplier of a rare critical mineral where its ESG credentials could command premium pricing on an already high margin product given geographical supply-risks.

For further information, listen to our SmallCapPix podcast with Karl Akueson, CEO of Switch Metals below.